EB5 visa: ‘Partial investment option can reduce financial burden,’ expert as US Golden visas get costlier

US to significantly raise fees for non-immigrant visas, including EB-5, impacting immigration polici...

April 3, 2024

Many Indian nationals are looking to obtain their U.S. Green Card but with the current administration’s recent crackdown on H-1B visas as well as the lengthy waiting lists for EB-2 and EB-3 visas, many Indians have had to look for an alternative green card to allow them to live the American Dream and work in the United States.

Because of this, the largely popular EB-5 Visa program has now become of extreme interest to Indian nationals. The number of Indians applying for the EB-5 Program is expected to more than double this year.

The growing demand for EB-5 has spread throughout India with many Indian citizens looking to invest with U.S. Immigration Fund from Hyderabad, Chandigarh, Punjab, Delhi, Mumbai, Pune, Bengaluru and more.

Founded in 2010, U.S. Immigration Fund is the largest EB-5 Regional Center Operator in the United States. With a 100% success rate on adjudicated projects, USIF provides opportunities for foreign investors and their families to obtain permanent U.S. residency through the EB-5 Visa Program by investing in U.S. real estate projects.

Founded in 2010, U.S. Immigration Fund is the largest EB-5 Regional Center Operator in the United States. With a 100% success rate on adjudicated projects, USIF provides opportunities for foreign investors and their families to obtain permanent U.S. residency through the EB-5 Visa Program by investing in U.S. real estate projects.

The EB-5 Program was created in 1990 by the U.S. Congress to allow foreign investors the opportunity to obtain their U.S. Green Card by investing in a U.S. business that will create jobs for Americans and benefit the economy.

The EB-5 Investor Visa Program enables residents of India to obtain their U.S. green card by investing a minimum of US $500,000 into a new commercial enterprise through a Regional Center, like U.S. Immigration Fund.

The EB-5 Program is one of the easiest and fastest ways to immigrate to the United States and many consider it the best alternative to the H-1B Visa for Indians.

Although a fast path to American citizenship, the process can still seem confusing for some Indian investors. Working with an experienced team like U.S. Immigration Fund gives the investor piece of mind.

The EB-5 Program was created in 1990 by the U.S. Congress to allow foreign investors the opportunity to obtain their U.S. Green Card by investing in a U.S. business that will create jobs for Americans and benefit the economy.

The EB-5 Investor Visa Program enables residents of India to obtain their U.S. green card by investing a minimum of US $500,000 into a new commercial enterprise through a Regional Center, like U.S. Immigration Fund.

The EB-5 Program is one of the easiest and fastest ways to immigrate to the United States and many consider it the best alternative to the H-1B Visa for Indians.

Although a fast path to American citizenship, the process can still seem confusing for some Indian investors. Working with an experienced team like U.S. Immigration Fund gives the investor piece of mind.

• One of the Fastest Ways to Immigrate to the U.S.

• No Visa Waiting List

• Investor & Family Members All Eligible For Green Cards

• Ability to Live and Move Anywhere in the U.S. at Any Time

• Flexibility to Work Anywhere or for Anyone in the U.S. or Start Your Own Company

• Lower Tuition Rates and Higher Acceptance Rates to College

• No Sponsorship Needed from Employer or Family Member

• No Education or Employment Requirements For Visa Process

• Direct Path to U.S. Citizenship after 5 Years of Permanent Residency (if the Investor Chooses)

• One of the Fastest Ways to Immigrate to the U.S.

• No Visa Waiting List

• Investor & Family Members All Eligible For Green Cards

• Ability to Live and Move Anywhere in the U.S. at Any Time

• Flexibility to Work Anywhere or for Anyone in the U.S. or Start Your Own Company

• Lower Tuition Rates and Higher Acceptance Rates to College

• No Sponsorship Needed from Employer or Family Member

• No Education or Employment Requirements For Visa Process

• Direct Path to U.S. Citizenship after 5 Years of Permanent Residency (if the Investor Chooses)

U.S. Immigration Fund is one of America’s leading EB-5 Regional Center Operators with world-renowned investment opportunities from across the United States.

6,000+ families are successfully investing with U.S. Immigration Fund to achieve their immigration dreams.

USIF has a 100% success rate on all adjudicated projects with thousands of 1-526 petitions approved, and I-829 petitions approved.

From concept to completion, U.S. Immigration Fund is there with you through the entire process. Having an experienced team of experts on your side helps to ensure the timely success of receiving permanent residency in the USA.

Strong Immigration Attorney Network

Selecting an immigration attorney to prepare the I-526 and I-829 petitions is equally as important as choosing the proper Regional Center and investment project. USIF has worked with several of the best immigration attorneys in the EB-5 industry to successfully process thousands of cases. These immigration attorneys are located in India and are able to meet with potential investors to answer any questions you may have.

Top Projects with the Best Developers

One of the core principles contributing to the success of USIF has been its ability to establish relationships with some of the largest developers in the United States that are responsible for shaping the skyline of New York City, Miami Beach, Los Angeles and more. Investing with proven companies that have long-standing track records of success on projects of similar scale and complexity provides great confidence to USIF and its investors.

Global Positioning

With offices, partnerships and representatives located throughout India in cities like Mumbai, Delhi, Bangalore, and Hyderabad, USIF is positioned to collaborate on a global scale. Our team of representatives, as well as third-party counsel, travel throughout India and the world on a regular basis to support, educate and inform potential clients on the nuances of the EB-5 Program and the investment projects available.

Our estimates at present indicate that the entire EB-5 process should take approximately 5 years for Indian citizens to complete. Based on current processing times by United States Citizenship and Immigration Services (“USCIS”), an Indian citizen should receive an I-526 approval in approximately 18 months. It will then take approximately 4-6 months for the Investor and his/her family to complete consular processing at a U.S. consulate in India or complete adjustment of status in the United States. After one year and nine months of holding conditional lawful permanent resident status, an Investor may file form I-829 to remove the conditions on his/her lawful permanent residence. The form I-829 petition must be filed with USCIS no later than the 2nd anniversary of the investor’s conditional lawful permanent resident status (this date appears on the conditional green card). Based on current processing times, an Indian citizen should receive an I-829 approval and unconditional green card within 18 to 24 months. USCIS anticipates processing times to improve as they hire additional adjudicators this year.

No. Unlike investors born in the People’s Republic of China, who have to wait approximately 3.5 years before receiving their conditional green card after an I-526 approval, Indian citizens are currently not subject to a visa waiting list.

Under the EB-5 visa program, an individual investor’s spouse and unmarried children under the age of 21 are allowed to receive green cards and accompany the investor to the U.S. as derivative beneficiaries. Each family member does not need to make a qualifying investment.

Under U.S. immigration law, parents of the EB-5 investor are not considered immediate relatives and therefore cannot accompany the investor to the United States as part of the investor’s family unit under one EB-5 visa process. Should the EB-5 investor choose to apply for U.S. citizenship after 5 years of holding permanent resident status, the investor could sponsor his/her parents for a family based green card as a U.S. citizen.

Generally, under U.S. tax laws, persons who become U.S. green card holders (lawful permanent residents), and people who spend at least one-half of each calendar year physically present in the U.S., are likely considered residents of the U.S. for tax purposes. The general rule of the U.S. tax system is that a person who is a U.S. tax resident is taxed on their worldwide income. Assets are not usually taxed unless income is generated on the asset or the asset is sold and a taxable financial gain results. The U.S. and India have entered into a Double Taxation Avoidance Agreement which seeks to minimize situations where people and companies are taxed both in the U.S. and India. Our law firm strongly recommends potential EB-5 investors to seek professional tax advice to address their individual tax situation and enable proper tax planning. Our law firm does not advise on U.S. taxation issues.

Lawful permanent resident (“LPR”) status is a residency permit that is intended to allow people to live in the United States on a long-term basis. It is not a tourist or visitor visa that is intended for short and sporadic visits to the United States. If a person holding LPR status spends significant amounts of time outside the United States, returning only for brief visits, it likely that they could encounter detailed questions when then seek to re-enter the U.S. from officers of U.S. Customs and Border Protection (“CBP”) to determine whether the person is complying with their status as a LPR. Generally, persons who hold LPR status should not engage in one trip lasting more than 6 months outside the United States.

If a person holding LPR status expects to travel for longer than 6 months outside the United States without returning, then many of our clients find it best to apply for a reentry permit from USCIS. The reentry permit is the strongest proof of one’s intention to remain an LPR in light of extended travel outside of the U.S. A reentry permit can be applied for prior to the LPR’s departure from the United States. Upon approval, the LPR holder obtains a passportstyle travel document issued by USCIS. Even if the LPR does not intend to be outside of the U.S. for a full year, our firm recommends that an LPR obtain a reentry permit if he/she intends to spend significant time outside of the U.S., e.g. more than 6 months per year.

US to significantly raise fees for non-immigrant visas, including EB-5, impacting immigration polici...

In an era of competitive global education and career opportunities, Indian students in the U.S. on F...

The EB-5 Reform and Integrity Act of 2022 reshapes the EB-5 visa program, impacting the minimum inve...

Jupiter, FL – Interest continues to increase for the EB-5 visa around the globe, and specifically ...

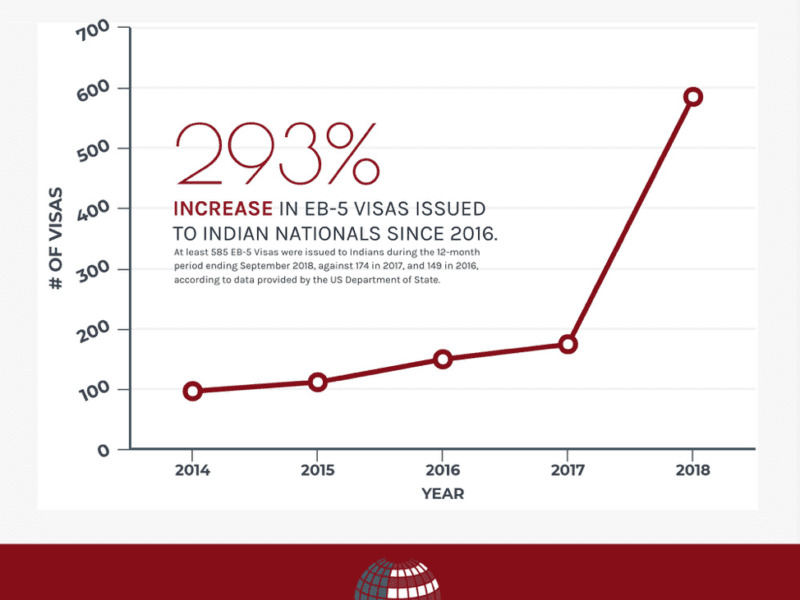

According to the US Department of State, the number of Indian citizens who have been issued EB-5 vis...

EB-5 visa applications soar in response to continual H-1B administration changes. Earlier this year ...

June 25, 2018 By: Harjit Singh There’s little security in an H-1B; quitting the company that spons...

By EB-5 Daily In just the past several months, the EB-5 Program has seen a dramatic increase in the ...

By Study International Staff | March 19, 2018 In the US, there is a visa programme that makes foreig...

As the H-1B visa program faces future uncertainty, especially under the Trump administration, many H...

Washington, D.C. – November 27, 2017: Having travelled to India frequently during the las...

Nov 07 NEW DELHI: US Immigration Fund has tied up with education firm The Chopras group to promote E...

Indian investors are pursing EB-5 immigrant investor visas in greater numbers than ever before. The...

The United States has historically been the most lucrative economy to migrate to for Indian students...

Here are all the benefits and important points about EB 5 visa program: Published: July 13, 2017 6:4...

AVAILABLE NOW?

Speak to your EB-5 immigration specialist on WhatsApp.

![]()

AVAILABLE NOW?

Speak to your EB-5 immigration specialist on WhatsApp.

![]()